8 Key Consumer Tech Trends for Entertainment

September 2, 2019

- Produced in Partnership by Consumer Technology Association and Variety Intelligence Platform

Highlights from CTA's U.S. Consumer Sales and Forecasts Report

Entertainment finds itself in the midst of digital disruption, which will be amplified once 5G internet begins to hit the mainstream. The trends included here illustrate shifts that are not only changing the consumption of entertainment, but also creating new distribution channels and devices to engage with content.

Older systems are being replaced by younger ones more suited to the new environment, but some previous generation systems are still surviving, even if on the decline. Others, like video games, have reinvented themselves and are generating more revenue than ever before.

With many elements of the industry changing, one essential thing remains the same: people haven’t stopped wanting to be entertained. This report highlights the main ways this will continue.

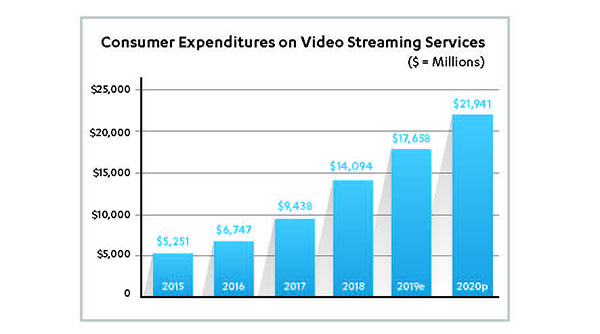

1. Subscription streaming video services continue to grow.

Video continues to comprise over two-thirds of the total revenue for subscription streaming services (music accounts for just under a third) and are predicted to keep increasing at a strong pace for 2020, up 24% to $21.9 billion.

The growth of subscription video is multifaceted, and not only credited to the rise of the original big three services, Amazon, Hulu and Netflix. With Netflix’s growth plateauing, the predicted market increase will come from elsewhere.

The growth of subscription video is multifaceted, and not only credited to the rise of the original big three services, Amazon, Hulu and Netflix. With Netflix’s growth plateauing, the predicted market increase will come from elsewhere.

A number of high-profile subscription streaming services will be debuting in the remainder of 2019 and 2020, namely Apple TV+, Disney+, HBO Max and NBCU’s unnamed service. These will help account for the steady rise in consumer expenditure within subscription video, as the number of major products available to consumers will more than double soon.

It is also important to note that there are several Streaming Video on Demand (SVOD) sports platforms out there for consumers to purchase. DAZN, ESPN+ and B/R Live all launched in 2018, joining NBC Sports Gold, among others. As networks increasingly migrate content onto their SVOD services, spending will increase as fans maintain access to their favorite sports and leagues.

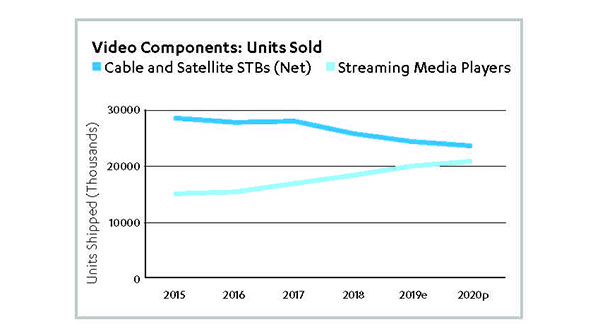

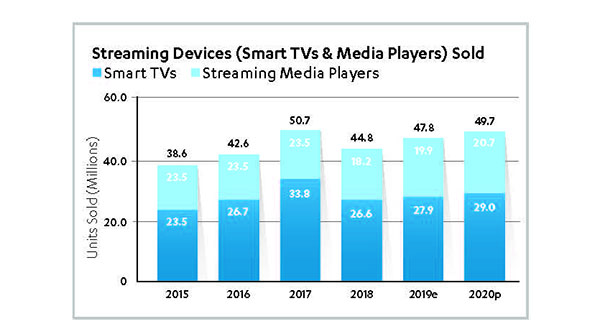

2. Streaming media players unit sales are catching up to traditional set-top boxes.

Satellite set-top boxes are experiencing a precipitous decline in units sold, and are predicted to fall in 2020 by 30% from levels seen in 2015. By comparison, cable boxes are only seeing moderate declines, down 4% from 2015. Together, traditional set-top boxes (STBs) are forecast to sell 23.7 million units in 2020. Streaming media players (SMPs) will see 20.7 million units sold.

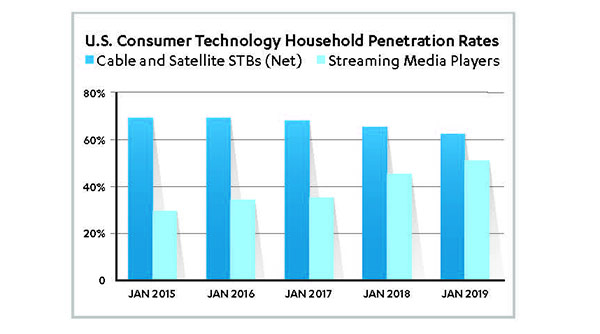

If sales patterns continue, it will be only a matter of time until SMPs sell more than STBs. In 2015, for every set-top box sold, there were 0.53 streaming media players. In 2020, that’s predicted to reach 0.87. SMPs are catching up, and this year crossed the threshold into majority status, in 51% of American households.

If sales patterns continue, it will be only a matter of time until SMPs sell more than STBs. In 2015, for every set-top box sold, there were 0.53 streaming media players. In 2020, that’s predicted to reach 0.87. SMPs are catching up, and this year crossed the threshold into majority status, in 51% of American households.

This doesn’t necessarily indicate a service swap. With Multichannel Video Programming Distributors (MVPDs) now offering some subscribers the option to stream channels via SMPs instead of STBs, some of the growth will be due to MVPD subscribers switching out their cable boxes for a Roku.

This doesn’t necessarily indicate a service swap. With Multichannel Video Programming Distributors (MVPDs) now offering some subscribers the option to stream channels via SMPs instead of STBs, some of the growth will be due to MVPD subscribers switching out their cable boxes for a Roku.

Others may find the interface of streaming media players easier to use for accessing free and subscription streaming services, despite STB manufacturer attempts to create single access devices.

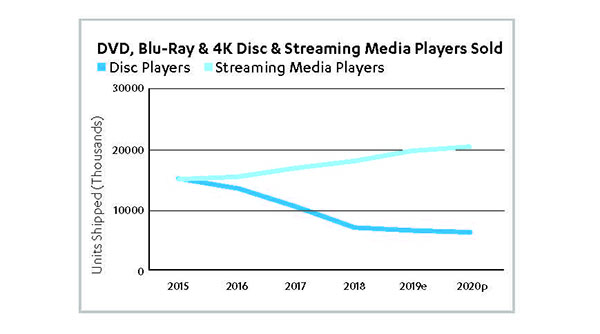

3. Streaming device sales have replaced disc players, but disc legacy remains.

CTA estimates there will be 3.3 streaming media players sold for every DVD/Blu-ray player sold in 2020. This number was 1.1 in 2016, and it represents the stunning shift in the consumption of streamed, mostly rented (either directly or via a subscription) content, versus the traditional ownership of a physical copy.

The number of streaming media players sold is estimated to continue to grow, by 4% in 2020 to 20.7 million. In contrast, 6.2 million disc players will be sold, suggesting there is still a market for physical copies of entertainment, even if it’s nowhere near what it was at its zenith.

The number of streaming media players sold is estimated to continue to grow, by 4% in 2020 to 20.7 million. In contrast, 6.2 million disc players will be sold, suggesting there is still a market for physical copies of entertainment, even if it’s nowhere near what it was at its zenith.

New sales of disc players may not represent an appetite to buy new discs, but the desire to play existing content without paying for it again. With the demise of UltraViolet, and because Vudu’s Disc to Digital conversion program is no longer available on non-Vudu platforms, the 64% of homes with a disc player remain without a cost-efficient way to convert fully to streaming.

4. Smart TVs continue to grow.

CTA predicts Smart TVs will make up 74% of all new TV sets sold in 2020, up 4% from the estimated total for 2019. The increase in ownership of these devices has grown from 24% of households in 2014 to 60% in 2019 and are expected to rise again in 2020.

There are more smart TVs sold per year than streaming media players, despite the latter being a much cheaper purchase. This suggests that consumers prefer integrated solutions and shows the wisdom in Roku and Amazon Fire making deals to embed in smart TVs from some manufacturers.

There are more smart TVs sold per year than streaming media players, despite the latter being a much cheaper purchase. This suggests that consumers prefer integrated solutions and shows the wisdom in Roku and Amazon Fire making deals to embed in smart TVs from some manufacturers.

The preponderance of streaming-capable devices in the home has three main effects on the current TV business:

- The growth in Connected TV (CTV) advertising

will continue as more and more people have the means to watch via CTVs or connected devices.

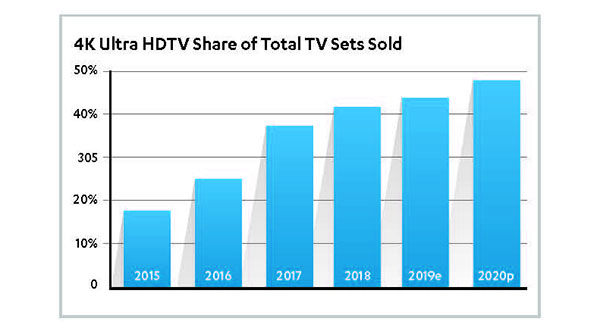

5. 4K is beginning to get big.

CTA predicts 4K Ultra High-Definition TVs (4K UHD) will make up almost 50% of new TVs sold in 2020, the highest proportion of sales in their history. This represents an increase of 10% on the estimated total for 2019, and it may be due to the average unit price falling for the second straight year.

In January 2019, more than one in three homes in the U.S. had a 4K TV, which is monumental growth considering only 1% had them in 2014. With this comes an increased demand for content available in 4K.

In January 2019, more than one in three homes in the U.S. had a 4K TV, which is monumental growth considering only 1% had them in 2014. With this comes an increased demand for content available in 4K.

Streaming services like Netflix, Amazon and Hulu; Transactional Video On Demand (TVOD) merchants like Apple; and video game console manufacturers Sony and Microsoft all offer 4K content. The holdout is traditional pay TV. If the pay TV providers are serious about keeping their remaining customers, matching the video output from their online rivals will be essential.

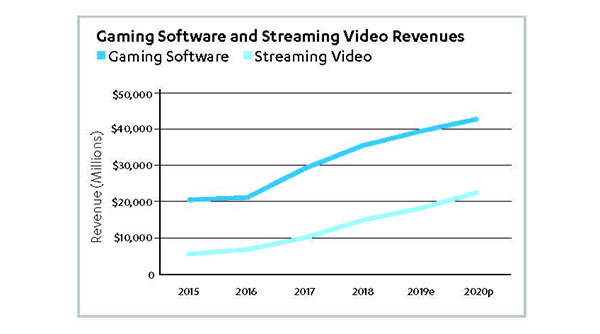

6. Gaming is bigger than you think.

Revenues from video game software continue to rise, with 2020 predicted to bring in double that seen in 2015. For context, the software gaming industry is estimated in 2019 to be 2.2 times as large as subscription streaming video.

In-game purchases have driven the increase in software spend since 2017 and now account for around a third of all gaming revenue. The amount spent is beginning to tail off, with only a 14% growth predicted for 2020, compared with the 92% seen in 2018.

In-game purchases have driven the increase in software spend since 2017 and now account for around a third of all gaming revenue. The amount spent is beginning to tail off, with only a 14% growth predicted for 2020, compared with the 92% seen in 2018.

The amount spent in total on actual games (downloaded and physical media) is fairly steady, with an expected 2% increase. Digital games continue to grow though, accounting for 5.7 times the spend versus physical discs. The growth in digital revenues is a boon for console manufacturers and developers, who have seen huge revenue streams emerge.

These earnings may ultimately be threatened by the arrival of new gaming subscription services. We are past the nascent stage, but with Google and Apple entering the subscription arena soon and the adoption of 5G internet, revenues generated from cloud-based gaming could soon blow up in a similar fashion to ingame purchases.

This could see more new entrants to the cloud gaming world, along with video game manufacturers and developers creating or significantly increasing their own subscriber products.

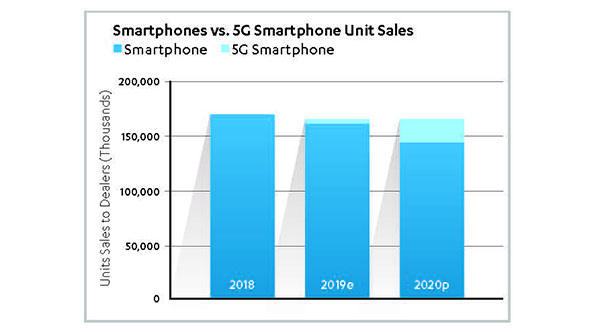

7. 5G is about to land.

Long promised, 5G internet is arriving. This will have an effect on three key areas: in-home internet, smartphones and entertainment.

In-home internet: Revenues from sales of home networking options, including Wi-Fi routers and wholehome solutions, broadband gateways and 5G home gateways, will total $5.3 billion in 2020.

Of this, 24% will be attributable to 5G devices. As well as representing homes free from the local cable/satellite monopoly, the majority of these homes will likely be heavy Internet of Things users, with advanced smart homes.

Of this, 24% will be attributable to 5G devices. As well as representing homes free from the local cable/satellite monopoly, the majority of these homes will likely be heavy Internet of Things users, with advanced smart homes.

Smartphones: 5G smartphones are predicted to boost the total number of smartphone sales in 2020. Levels will remain below the 2018 high, as consumers tend to keep their handsets for longer.

Of smartphones sold in 2020, 12% will be 5G handsets. Those early adopters will not be spending the extra money on a handset just for show. They will use the lightning-fast speed to drive demand for the emerging cloud-based technologies, most notably playing video games, which used to be limited to consoles or highend PCs via the cloud.

Entertainment: 5G networks will have an impact upon all aspects of entertainment. As 4K UHD content becomes more common, 5G download speeds means mobile viewers will not have to settle for a downgrade in quality as they watch. 5G will also mean that cloudbased subscription gaming services don’t have to be tethered to the home.

Virtual and augmented reality (VR/AR)-based technology will be boosted by the rise of 5G, as download lag times vanish. For handset users, better battery life will be a necessity, and could become a liability for manufacturers known for quick performance declines in new batteries.

8. VR and AR may finally realize their potential.

The growth in VR/AR eyewear stalled in recent years, following the high of 2016. Growth rates either declined or were sluggish in the years since, but 2020 is predicted to see double-digit growth for the first time in four years.

This is no doubt in part to the emergence of 5G, which makes for a better VR experience due to the reduction in loading times. VR growth has also been aided by the introduction of all-in-one headsets, which don’t require connections to video game consoles or high-end PCs.

This is no doubt in part to the emergence of 5G, which makes for a better VR experience due to the reduction in loading times. VR growth has also been aided by the introduction of all-in-one headsets, which don’t require connections to video game consoles or high-end PCs.

But VR headsets may remain a niche product, even with 5G. Currently in 15% of homes, they remain expensive (with an average retail price of $349) and cumbersome, being a piece of equipment strapped over the head.

The real boost may be for AR. Increased internet speeds means post-2020 may see a real boost in AR adoption. Areas such as retail, which may use AR to project new clothes onto the user, and beauty could be first adopters of the tech from a consumer standpoint, as could TV shows and advertisers, with AR offering new ways for consumers to interact with a show or brand.

Conclusion

The year 2020 looks set to be another year of disruption for established media and entertainment companies. The emergence of new distribution channels and entertainment formats will create opportunities for innovative new entrants to disturb once-locked markets.

In particular, the potential that 5G will bring as its adoption grows will present the right set of circumstances for forward-thinking companies to become one of the first to market in areas which are set to boom in the coming years (AR, subscription gaming, 4K mobile video distribution).

Opportunities will be available for anyone willing to adapt to the new normal, unlike traditional media’s track record in the 2010s. Understanding the consumer trends within entertainment which point to money-making potential will become even more essential.

Learn More

To learn more, see the full U.S. Consumer Technology Sales and Forecasts report at CTA.tech/salesandforecasts.

To find out more about Variety Intelligence Platform, please visit variety.com/vip-sample.

Consumer Technology Association (CTA)®

The Consumer Technology Association is the trade association representing the $401 billion U.S. consumer technology industry, which supports more than 18 million U.S. jobs. More than 2,000 companies — 80 percent are small businesses and startups; others are among the world’s best known brands — enjoy the benefits of CTA membership including policy advocacy, market research, technical education, industry promotion, standards development and the fostering of business and strategic relationships. The Consumer Technology Association also owns and produces CES® — the world’s gathering place for all who thrive on the business of consumer technologies. Profits from CES are reinvested into CTA’s industry services. Visit CTA.tech to learn more.

![]()

Variety Intelligence Platform

Variety Intelligence Platform (VIP) is a new service soon to come from Variety. With in-depth reports focusing on the key trends and topics across entertainment, as well as immediate analysis and commentary on the biggest stories impacting the industry, VIP will be a must-have for executives who seek to understand entertainment and media. Visit Variety.com/VIP-sample to learn more.